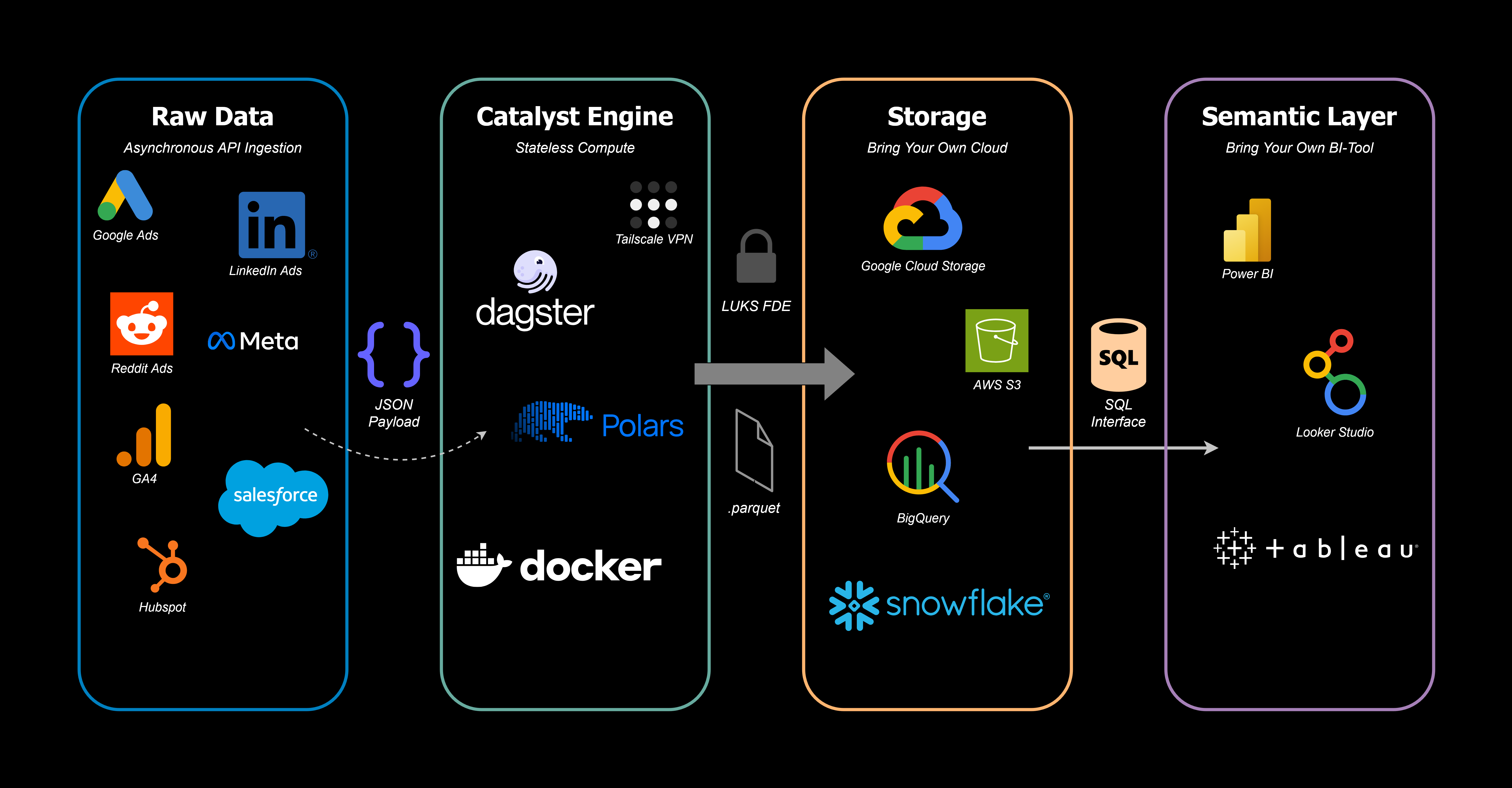

1. Asynchronous API Ingestion

Catalyst is built to absorb network chaos. It autonomously extracts JSON payloads from a complex web of external APIs, including Google Ads, Meta, Salesforce, and HubSpot.

Catalyst is a single-tenant data engine engineered to process complex telemetry at scale. By decoupling stateless compute from long-term storage, it delivers deterministic performance, self-healing orchestration, and complete architectural ownership.

Scaling a traditional, coupled data warehouse usually means skyrocketing cloud costs. Managed SaaS vendors charge extra for every new API connector. They force you to keep massive compute clusters idling 24/7 just to access your historical data. On top of the bloat, standard pipelines remain highly fragile, often breaking under network microbursts and API rate limits.

Catalyst resolves this through first-principles engineering. By isolating the expensive heavy lifting to out-of-core tools and routing the final outputs to your existing cloud storage, you get the speed of a dedicated server with the infinite scale of a hyperscaler.

I build the engine. You own the metal. Catalyst operates as a stateless processing node that sits between your raw data and your semantic layer.

.parquet files and routed directly into your Google Cloud Storage, AWS S3, BigQuery, or Snowflake instances. You own the storage; you own the data.

To demonstrate the payload capacity of the Compute Engine, I built a fully autonomous, B2B multi-channel reporting suite. It bypasses off-the-shelf SaaS connectors to prove that this architecture can gracefully digest the chaos of multiple ad network APIs and output crystal clear, AI-augmented signals.

Whether you need a dedicated data warehouse, custom engineering for your startup, or complex event processing, the deployment process is identical.

I review your current telemetry, API bottlenecks, and infrastructure targets to ensure complete platform coverage.

I provision your dedicated bare-metal environment, establish the Tailscale mesh, and compile the out-of-core orchestrator.

I deliver a deterministic, self-healing data pipeline. I maintain the architecture; your engineers build on top of it.